Share Deal vs Asset Deal Immobilien expert comparison

Real estate professionals weigh Share Deal vs Asset Deal Immobilien for property transactions. Understand key differences, tax impacts, and risks.

From years operating within the European and, specifically, German real estate market, it’s clear that acquiring property is rarely a simple deed transfer. Investors and developers frequently face a fundamental choice: purchase the shares of a company owning the property, or buy the property directly. This decision, between a share deal and an asset deal, carries significant implications for legal structure, taxation, and potential liabilities. My experience shows that what seems like a minor structural difference can drastically alter a project’s financial outcome and operational complexities.

Overview

- Share Deal vs Asset Deal Immobilien represents two distinct legal approaches to real estate acquisition.

- A share deal involves buying the company that owns the property, acquiring its shares.

- An asset deal directly purchases the physical property itself, along with associated rights and obligations.

- Tax implications vary significantly between the two, impacting transfer taxes, corporate income tax, and depreciation.

- Liability transfer is a critical differentiator; share deals assume historical company liabilities.

- Due diligence processes differ in scope and intensity for each transaction type.

- Flexibility in financing and post-acquisition restructuring is influenced by the chosen method.

- The transaction structure can affect closing timelines and legal costs.

Understanding the Core Differences in Share Deal vs Asset Deal Immobilien

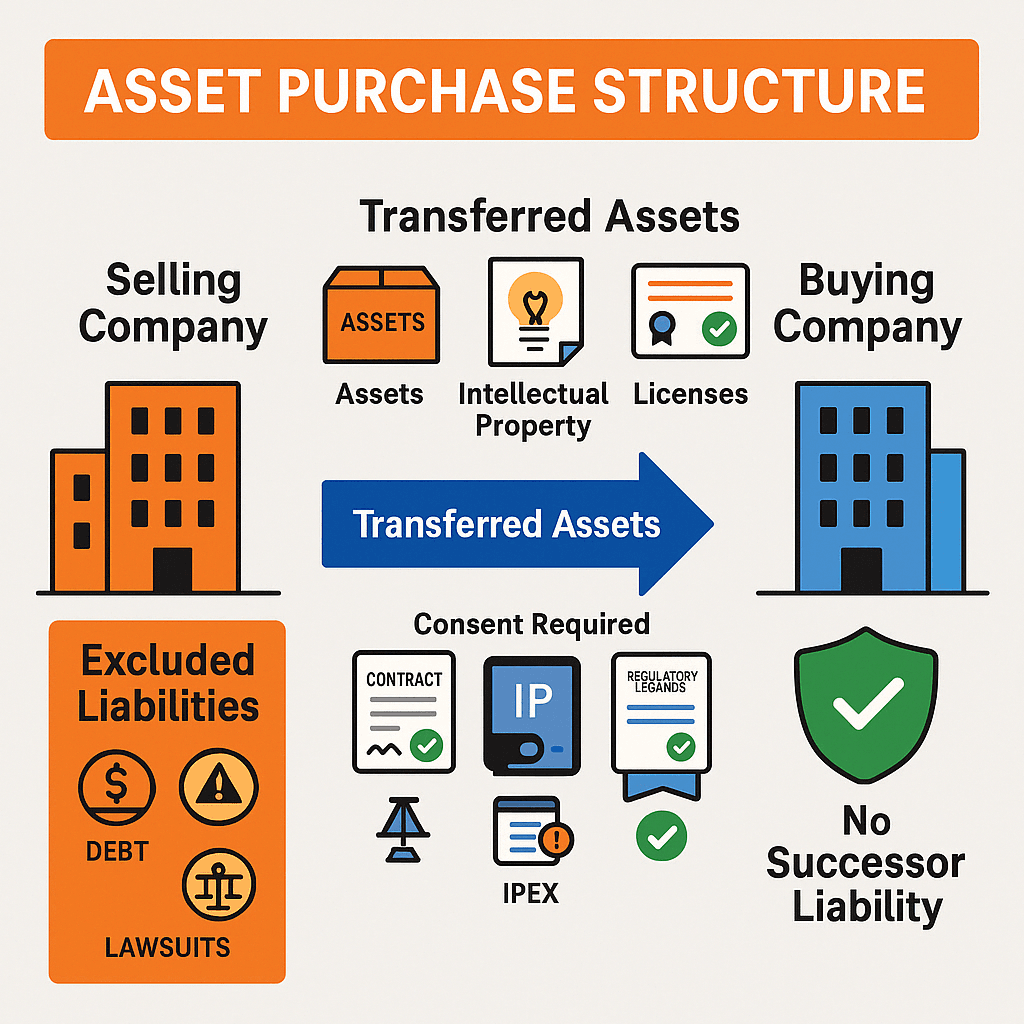

When acquiring real estate, the choice between a share deal and an asset deal is foundational. In a share deal, the buyer purchases the shares of a legal entity, typically a GmbH in Germany, that holds the property. The property itself remains with the existing company. The ownership of the company changes hands. This means the buyer acquires all assets and liabilities of that company, whether known or unknown.

Conversely, an asset deal involves the direct purchase of the physical real estate asset. This includes the land and buildings. The seller’s legal entity retains its corporate identity; it simply divests a specific property. Here, the buyer acquires only the identified assets and specific liabilities explicitly agreed upon. The property’s title passes directly to the new owner. Each approach carries unique characteristics that shape the entire transaction process.

Legal and Tax Implications of Share Deal vs Asset Deal Immobilien

The legal and tax landscape significantly diverges for Share Deal vs Asset Deal Immobilien. In an asset deal, property transfer tax (Grunderwerbsteuer) is almost always incurred. This is a substantial cost in Germany, often ranging from 3.5% to 6.5% of the purchase price, depending on the federal state. Depreciation rules also apply to the acquired asset directly. The buyer can often step up the basis of the property for tax purposes.

For a share deal, property transfer tax might be avoided or reduced under specific conditions. If less than 95% of the shares of a property-owning company are transferred to a single buyer or a group of buyers acting in concert, no property transfer tax is triggered. However, strict rules apply. Corporate income tax and trade tax liabilities of the acquired company become the buyer’s responsibility. In the US, similar distinctions exist regarding stock purchases versus asset purchases, with varying state and federal tax consequences. Understanding these specific national nuances is crucial.

Due Diligence and Risk Assessment in Share Deal vs Asset Deal Immobilien

The scope of due diligence fundamentally shifts between an asset purchase and a share purchase. In an asset deal, due diligence primarily focuses on the physical property itself. This includes its legal title, environmental status, structural integrity, and existing leases. The buyer assesses the asset’s specific risks and liabilities. This process is generally more straightforward, isolating the property from the seller’s broader business.

For a share deal, due diligence must be far more extensive. The buyer is acquiring an entire company, including its historical baggage. This means scrutinizing not only the property but also the company’s entire legal, financial, environmental, and tax history. Any past legal disputes, undeclared tax liabilities, or environmental contaminations associated with the company become the buyer’s responsibility. This necessitates a much deeper dive into corporate records and potential hidden risks, making due diligence in Share Deal vs Asset Deal Immobilien a complex endeavor.

Strategic Considerations for Property Acquisitions

Selecting between these two transaction types extends beyond immediate tax savings; it involves broader strategic thinking. An asset deal offers cleaner acquisition. The buyer gains a defined asset without inheriting the seller’s corporate history. This method is often preferred for single properties or when the seller has significant unrelated liabilities. It provides greater certainty regarding future obligations.

A share deal can be advantageous for portfolio acquisitions or when existing contracts tied to the corporate entity are critical. It can streamline the transfer of permits, licenses, and long-term lease agreements. However, it demands a higher degree of trust and thorough vetting of the target company. The potential for hidden liabilities requires robust indemnities and warranties from the seller. The ultimate choice depends on the specific property, the seller’s structure, and the buyer’s risk appetite and investment goals.